Overview

- Employer contributions to a superannuation fund for the benefit of an employee, or for a person deemed to be an employee are “wages” for payroll tax purposes.

- Superannuation contributions for the benefit of a director of a company or a member of the board of management of an incorporated or unincorporated association are “wages”.

- Superannuation contributions by an employer to a defined benefits fund are “wages”.

- Employee contributions to a superannuation fund out of after-tax wages are not “wages”.

- Superannuation contributions relating to underpaid wages are payable for payroll tax purposes when the wages are paid.

- Payments of SGC are subject to payroll tax when a Superannuation Guarantee Statement is lodged with the Australian Taxation Office (ATO) or when the ATO reassesses an SGC.

- Additional payments by employers to employees as compensation for late payment of wages or superannuation contributions (other than additional superannuation contributions) are not “wages” for payroll tax purposes.

- Additional superannuation contributions paid by an employer as compensation for late payment of wages or superannuation are “wages” for payroll tax purposes.

Commissioner's Practice Note

Employer superannuation contributions are “wages” for payroll tax purposes

Employer superannuation contributions paid or payable by an employer in respect of an employee are “wages” for payroll tax purposes under Division 3 of Part 3 of the Act, and include contributions:

- to a superannuation fund, including a defined benefits fund;

- as a superannuation guarantee charge;

- to a provident or retirement fund or scheme;

- under a salary sacrifice arrangement;

- as a lump sum paid in respect of a class of employees;

- as any other form of superannuation.

Superannuation contributions are taken (“deemed”) to be “wages” when they are paid or become payable:

- by a third party for the benefit of an employee of the employer;

- for the benefit of a person taken to be an employee under a relevant contract;

- by an employment agent for the benefit of a person taken to be an employee under an employment agency contract.

Superannuation contributions paid or payable by a company to or in relation to a director of the company are “wages” for payroll tax purposes if provided as remuneration for services as a director. “Company” has an extended meaning under s.3(1) of the Act, and includes all incorporated and unincorporated bodies, and partnerships. Therefore, superannuation contributions paid or payable as remuneration in relation to a member of the board of management of such bodies are also “wages”.

Employer contributions to defined-benefit funds are “wages”

Employer contributions to a defined-benefit fund are generally determined having regard to regular actuarial valuations, including calculation of the employer’s contribution required to meet the accrued cost of future benefits for existing members of the fund.

Payments by an employer to a defined-benefit fund are “wages” for payroll tax purposes. This includes top-up payments to make up a deficit in the fund, to the extent the deficit is attributed by an actuary to services performed after 30 June 1996. For more information regarding contributions to defined benefits schemes, read Revenue Ruling PTA 040.

After-tax contributions by employees are not “wages”

If an employee makes superannuation contributions from wages after income tax contributions have been deducted, including contributions to a fund administered by the employer, the contributions are not “wages” under Division 3 of Part 3 of the Act.

Payroll tax on superannuation contributions when wages are under-paid

If an employer pays additional wages to an employee as a result of under-paying wages that were payable in a previous financial year, the employer may be liable to pay an additional superannuation contribution to the employee’s superannuation fund. An additional superannuation contribution is required if the additional wage payment increases the employee’s ordinary time earning as defined in s.6(1) of the Commonwealth Superannuation Guarantee (Administration) Act 1992 (“the SGA Act”).

For payroll tax purposes, payroll tax liability on the underpaid wages arises when the wages are paid or become payable, whichever occurs first. Therefore, underpaid wages are taxable in the financial year in which the wages should have been paid.

However, awards and enterprise agreements generally require employers to make superannuation contributions in accordance with the SGA Act. Under the SGA Act the additional superannuation contributions are required to be paid when the underpaid wages are actually paid. Consequently, additional superannuation contributions are payable when the additional wages are paid, and therefore must be included in the employer’s payroll tax return for the month or financial year in which the contributions are paid [1].

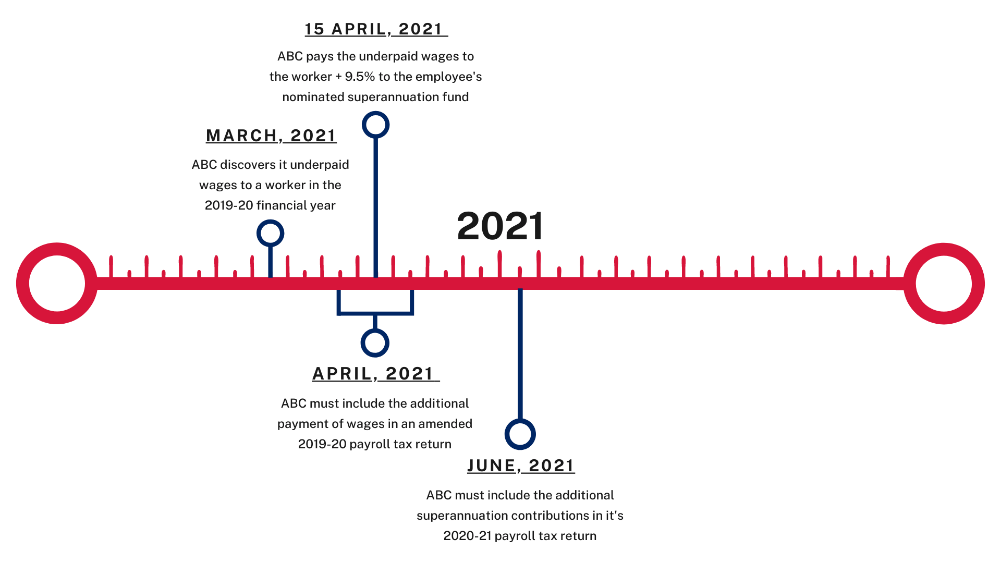

Example 1: Superannuation contribution on under-paid wages

In March 2021 ABC discovers that it underpaid wages to a worker in the 2019-20 financial year because it failed to pay the correct hourly rate under the relevant award. ABC pays the underpaid wages to the employee on 15 April 2021.

The additional payment of wages increases the “ordinary time earnings” of the employee. Therefore, ABC also makes an additional payment of 9.5% of the under-paid wages to the employee’s superannuation fund on 15 April 2021, as required under the SGA Act.

ABC is required to include the additional payment of wages in an amended payroll tax return for the 2019-20 financial year, but the payment of the additional superannuation contribution must be included in its 2020-21 payroll tax return.

Payroll tax on an SGC

Payroll Tax liability arises when a Superannuation Guarantee Statement (SG Statement) is lodged because the SGA Act provides that an SGC becomes payable on the day that the employer lodges an SG Statement [2]. An employer may self-assess a shortfall, or the ATO may issue a default assessment if the employer fails to do so.

If a default SGC assessment is issued by the ATO, the SGC is taken to be payable on the date on which the default assessment is made [3].

If an amended SGC assessment is issued by the ATO, resulting in an increase in SGC payable by the employer, the amended amount of SGC is taken to have become payable on the date of the original assessment [4].

ATO Information about the SGC can be found here:

When must an SGC be included in the employer’s payroll tax return?

An employer who lodges an SG Statement must include the SGC in its payroll tax return for the month or financial year in which the SG Statement was lodged.

This is the case even if the employer does not pay the SGC at the time the SG Statement is lodged, or if the SGC is paid to the ATO in instalments.

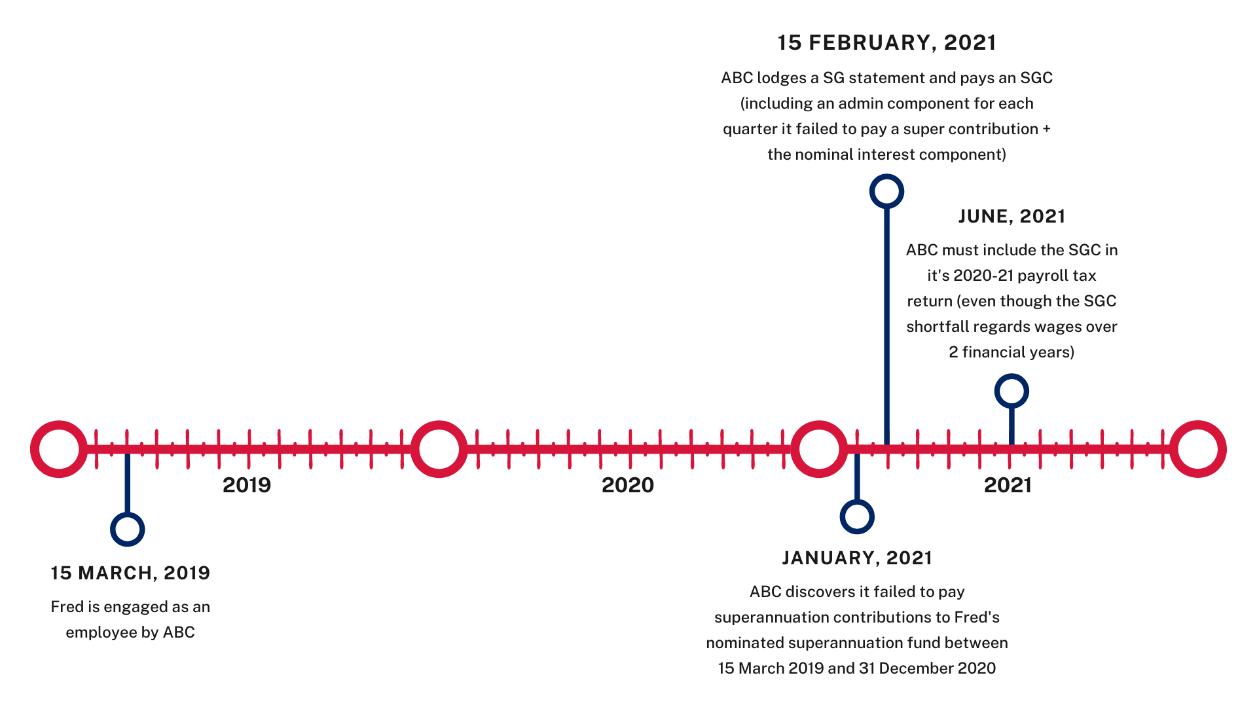

Example 2: Payroll tax payable on an SGC when SG Statement is lodged

On 15 March 2019 Fred was engaged as an employee by ABC. In January 2021 ABC discovers that it failed to pay superannuation contributions to Fred’s nominated superannuation fund for the period of 15 March 2019 to 31 December 2020.

ABC lodges a SG Statement and pays an SGC on 15 February 2021. The SGC includes an administration component for each quarter that it failed to pay a superannuation contribution, in accordance with s.32 of the SGA Act, plus the nominal interest component at rates specified in Regulations made under s.31 of the SGA Act.

Although the SGC Shortfall relates to wages paid over 2 financial years, ABC must include the SGC in its 2020-21 payroll tax return.

If the ATO reassesses the amount of SGC returned by an employer and the SGC payable by the employer is increased, the increase in SGC is taken to have been payable on the date the employer lodged its SG Return [5]. The employer may therefore be liable for penalty tax and interest under the TAA on the increased amount of SGC.

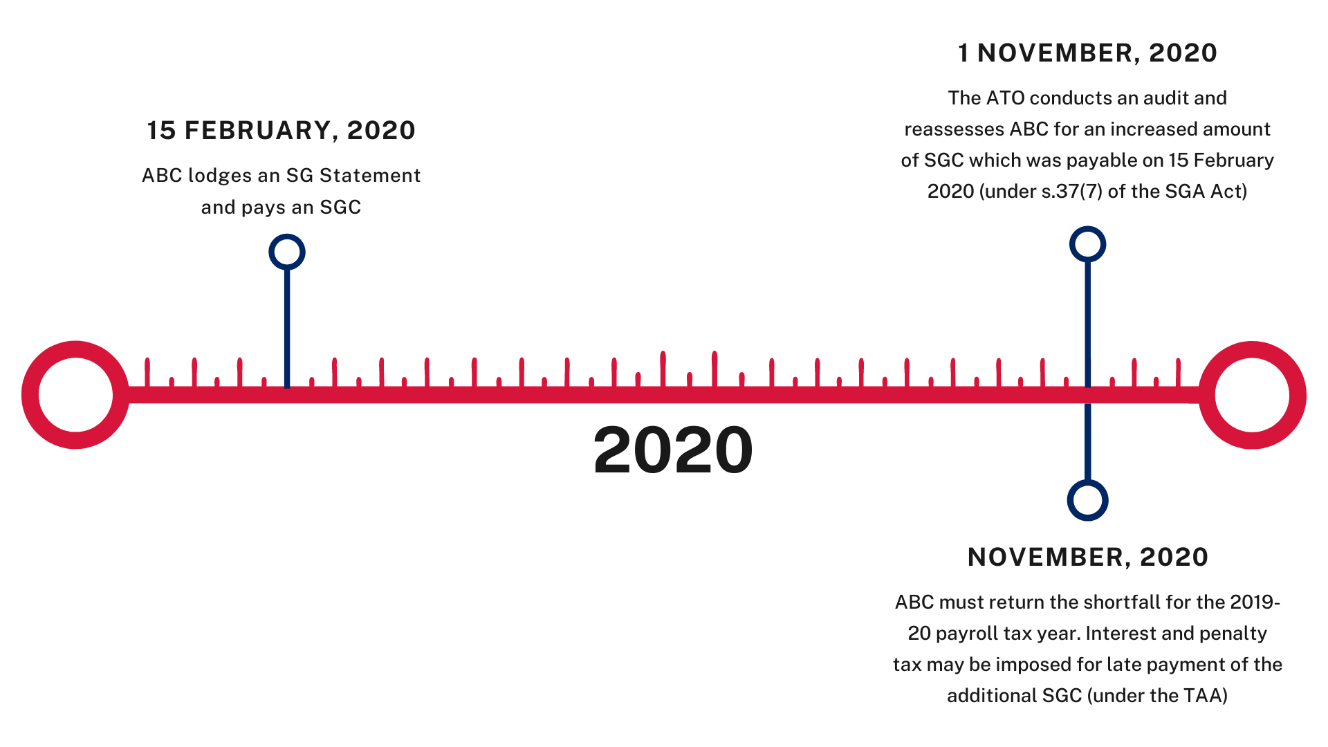

Example 3: Payroll tax payable on an SGC when reassessed by ATO

ABC lodges an SG Statement and pays an SGC on 15 February 2020. The ATO conducts an audit and on 1 Nov 2020 reassesses ABC for an increased amount of SGC. Under s.37(7) of the SGA Act the additional SGC was payable on 15 February 2020.

ABC must return the shortfall for the 2019-20 payroll tax year, and interest and penalty tax under the TAA may be imposed for late payment of the additional SGC

Compensation for late payment of wages and superannuation

If an employer pays an additional amount to an employee as compensation for the late payment of wages and/or superannuation, the compensation is not “wages” under s.13 of the Act and therefore is not subject to payroll tax, even if the employee uses the compensation to make an additional superannuation contribution. However, employers must maintain records that prove to the satisfaction of the Chief Commissioner that a payment is compensatory in nature and is not ordinary wages.

If an employer makes an additional contribution to the employee’s superannuation fund, the additional superannuation contribution is “wages” under Division 3 of Part 3 of the Act, and is therefore subject to payroll tax even if it is compensation for late payment of wages or late payment of superannuation contributions.

Australian Tax Office (ATO) amnesty for SGC payments

In 2020 the ATO offered an amnesty for employers who had failed to pay the SGC as a result of failing to pay the correct superannuation contributions to an employee’s correct superannuation fund (called a “Shortfall”). Applications for the amnesty closed on 7 September 2020.

Under the amnesty, employers are required to lodge a SG Statement and pay the SGC comprising the Shortfall plus nominal interest, to the ATO, but do not have to pay the quarterly administrative charge.

If an employer’s application for the amnesty is approved by the ATO and an SG Statement is lodged, the SGC, which includes the nominal interest component, must be returned for payroll tax purposes in the employer’s payroll tax return for the year in which the SG Statement was lodged with the ATO.

If the employer enters into an instalment arrangement with the ATO, the SGC must still be included in the employer’s payroll tax return for the financial year in which the SG Statement was lodged with the ATO.

Interest and penalty tax is not payable under the TAA unless the employer fails to pay payroll tax when an SG Statement is lodged with the ATO.

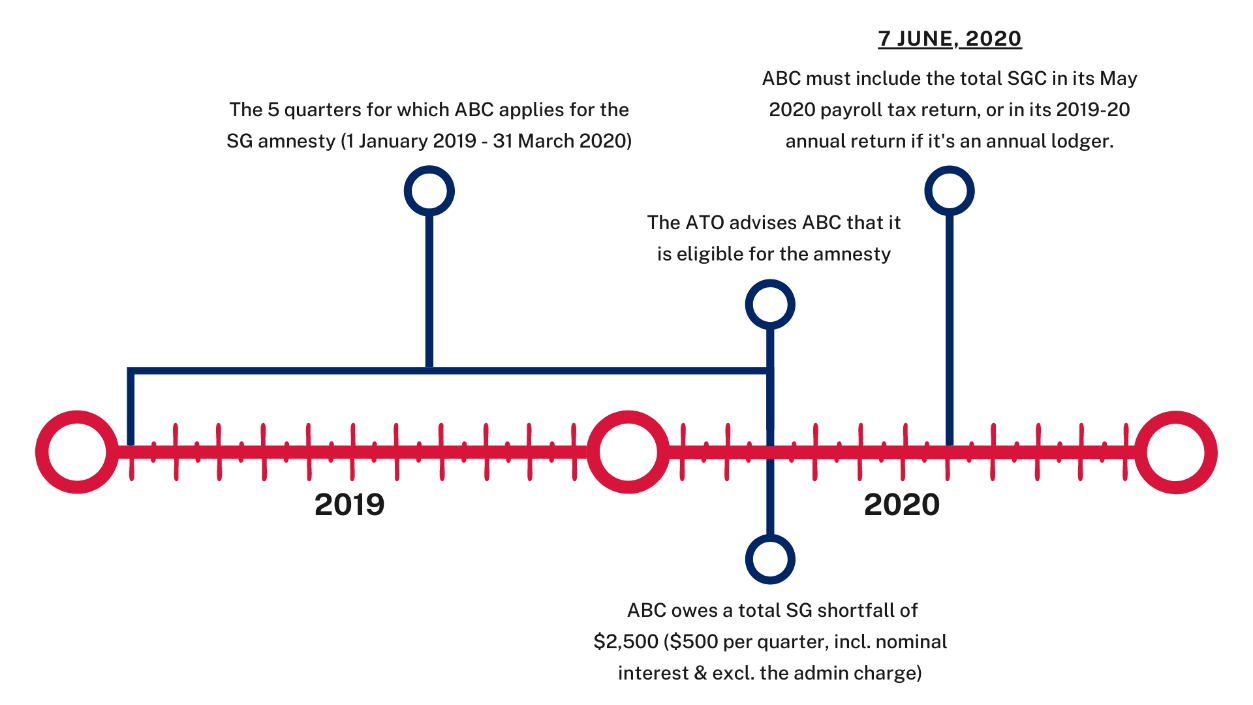

Example 4:Payment of payroll tax on an SGC paid under the ATO amnesty

ABC applies for the SG amnesty for five quarters from 1 January 2019 to 31 March 2020. The ATO advises ABC that it is eligible for the amnesty. The amount of SG shortfall that ABC owes is $500 per quarter, a total of $2,500 (including nominal interest but excluding the administration charge). ABC lodges an SG Statement and pays the SGC on 15 May 2020.

ABC must include the total SGC of $2,500 in its payroll tax return for May 2020 (due on 7 June), or in its annual return for 2019-20 if it is an annual lodger.

Note: If ABC only pays part of the SGC when it lodges the SG Statement and enters into an instalment arrangement with the ATO for payment of the balance, the whole of the SGC must still be included in its payroll tax return for 2019-20, not just the amount initially paid.

Footnotes

- ^ A monthly lodger must include an SGC in its return for the month in which the SG Statement is lodged. An annual lodger must include an SGC in its return for the financial year in which the SGC lodged.

- ^ See s.46 of the Superannuation Guarantee (Administration) Act 1992.

- ^ See s.36(3) of the Superannuation Guarantee (Administration) Act 1992.

- ^ See s.37(7) of the Superannuation Guarantee (Administration) Act 1992.

- ^ See s.37(7) of the SGA Act.